Foreign Currency Non-Resident Bank (FCNR(B)) Deposits: Strengthening India’s External Sector and Banking Liquidity

Foreign Currency Non-Resident Bank (FCNR(B)) Deposits: Strengthening India’s External Sector and Banking Liquidity

In an era of increasing global financial integration, countries continuously seek reliable sources of foreign capital to strengthen their external sector and maintain macroeconomic stability. For India, the overseas Indian community has emerged as a significant contributor to foreign exchange inflows through investments, remittances, and deposits. Among the various financial instruments available to Non-Resident Indians (NRIs), Foreign Currency Non-Resident Bank [FCNR(B)] deposits occupy a unique position because they attract foreign currency into the Indian banking system while protecting depositors from exchange-rate fluctuations.

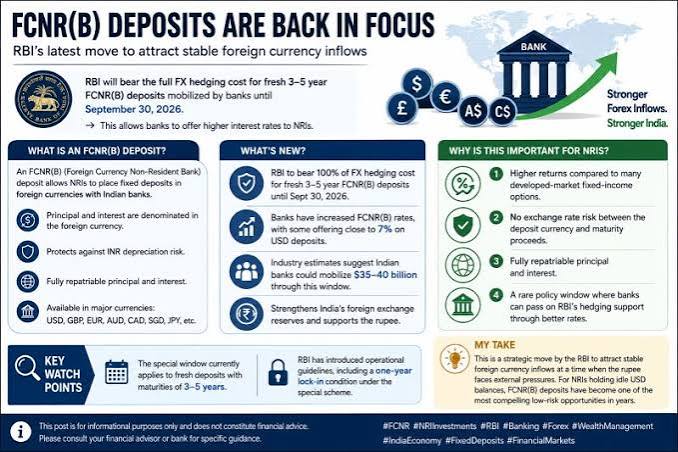

Recognizing the importance of these deposits, the Reserve Bank of India (RBI) has introduced a dedicated foreign exchange swap facility for fresh long-term FCNR(B) deposits mobilized up to September 30, 2026. By absorbing the entire hedging cost associated with these deposits, the RBI seeks to encourage foreign currency inflows, improve liquidity conditions in the banking sector, and provide stability to the Indian Rupee amid uncertain global economic conditions. The initiative reflects a proactive approach to strengthening India's external financial position without increasing sovereign debt obligations.

Understanding FCNR(B) Deposits

FCNR(B) deposits are term deposits maintained in designated foreign currencies with authorized Indian banks. Unlike conventional deposits that are denominated in Indian Rupees, these accounts are held directly in foreign currencies such as the US Dollar (USD), Euro (EUR), British Pound Sterling (GBP), Japanese Yen (JPY), Canadian Dollar (CAD), and Australian Dollar (AUD).

These accounts are available exclusively to Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs). The defining feature of FCNR(B) deposits is that both the principal amount and the interest earned remain in the chosen foreign currency throughout the tenure of the deposit. Consequently, depositors remain insulated from depreciation in the value of the Indian Rupee.

The tenure of FCNR(B) deposits generally ranges from one to five years. At maturity, the depositor receives the principal and accumulated interest in the same foreign currency, eliminating exchange-rate uncertainty and making the product attractive for long-term savings and wealth preservation.

Why the RBI Introduced the New Swap Window

The RBI's latest measure comes against the backdrop of evolving global financial conditions characterized by volatile capital flows, geopolitical uncertainties, changing monetary policies in advanced economies, and fluctuations in global interest rates. Such developments can exert pressure on emerging-market currencies, including the Indian Rupee.

To strengthen foreign exchange inflows, the RBI has adopted a strategy reminiscent of the measures employed during the currency volatility witnessed in 2013. Under the new framework, banks mobilizing eligible FCNR(B) deposits can access a special swap facility through which foreign currency deposits are exchanged with the RBI for Indian Rupees.

A key feature of the arrangement is the RBI's decision to absorb the hedging cost, estimated at approximately 2.8–3.5 percent annually. Normally, these costs reduce the attractiveness of FCNR(B) deposits for banks. By removing this burden, banks can offer more competitive returns to overseas depositors, thereby increasing the likelihood of attracting substantial foreign currency resources into the Indian financial system.

Key Regulatory Incentives and Relaxations

The RBI has complemented the swap facility with several regulatory concessions aimed at encouraging banks to actively mobilize FCNR(B) deposits.

One major relaxation is the exemption granted to incremental FCNR(B) deposits from the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements. Under normal circumstances, banks must set aside a portion of deposits as reserves, which limits the funds available for lending and investment. The exemption allows banks to deploy a larger share of mobilized resources productively.

In addition, liabilities arising from the swap transactions are excluded from banks' Net Open Position Limits (NOPL), reducing regulatory constraints related to foreign exchange exposure management.

To ensure financial stability, however, safeguards have been incorporated into the framework. Depositors must observe a minimum one-year lock-in period before premature withdrawal is permitted. Furthermore, participating banks cannot terminate swap agreements with the RBI before maturity. These provisions help prevent speculative behavior and ensure the long-term effectiveness of the scheme.

Benefits for Non-Resident Depositors

FCNR(B) deposits provide several advantages that make them one of the most preferred savings instruments for overseas Indians.

The most significant benefit is protection from currency risk. Since deposits are maintained and repaid in the same foreign currency, investors are shielded from losses that may arise due to depreciation of the Indian Rupee. This feature offers certainty regarding future returns and preserves the real value of savings.

Another important advantage is complete repatriability. Both the principal and interest can be transferred abroad without restrictions, enabling investors to maintain financial flexibility across jurisdictions.

Tax efficiency further enhances the attractiveness of FCNR(B) deposits. Interest earned on these deposits is exempt from income tax in India, thereby increasing the effective yield for depositors. Additionally, the deposits provide a secure investment avenue backed by India's regulated banking system, making them suitable for risk-averse investors seeking stable returns.

Impact on Foreign Exchange Reserves and Rupee Stability

One of the most important macroeconomic benefits of FCNR(B) deposits is their contribution to India's foreign exchange reserves. Every fresh deposit mobilized under the scheme brings additional foreign currency into the country, strengthening the reserve position of the economy.

Higher foreign exchange reserves improve India's ability to manage external shocks, meet international payment obligations, and withstand episodes of global financial stress. A strong reserve buffer also enhances investor confidence by demonstrating the country's capacity to meet its external commitments.

Moreover, increased reserve accumulation provides the RBI with greater flexibility to intervene in foreign exchange markets whenever excessive volatility threatens the stability of the Rupee. Consequently, FCNR(B) inflows indirectly contribute to exchange-rate stability and help moderate sudden currency fluctuations.

Contribution to Banking Sector Liquidity and Credit Growth

Beyond reserve accumulation, FCNR(B) deposits play a critical role in supporting liquidity within the domestic banking system. Through the RBI's swap mechanism, banks can convert foreign currency deposits into Indian Rupees and utilize the proceeds for domestic operations.

This process generates an additional source of liquidity at a time when credit demand may outpace the growth of domestic deposits. The availability of supplementary funds enables banks to maintain lending activity across productive sectors of the economy, including infrastructure, manufacturing, services, agriculture, and small enterprises.

Improved liquidity conditions also help reduce funding pressures within the banking system and support the smooth transmission of monetary policy. As a result, FCNR(B) deposits contribute not only to external stability but also to domestic economic growth.

FCNR(B) Deposits as a Non-Debt Source of Capital

An important policy advantage of FCNR(B) deposits is that they represent a non-debt-creating source of foreign capital from the perspective of the sovereign government. Unlike external commercial borrowings or sovereign bonds, these deposits are liabilities of commercial banks rather than obligations of the Government of India.

This distinction allows the country to strengthen its external financial position without increasing sovereign external debt. Consequently, FCNR(B) inflows help improve capital availability while preserving fiscal sustainability and reducing dependence on potentially volatile portfolio investments.

Furthermore, the relatively stable nature of NRI deposits makes them a valuable component of India's overall external financing strategy, particularly during periods of global uncertainty.

Challenges and the Way Forward

While FCNR(B) deposits offer significant benefits, policymakers and banks must remain mindful of certain challenges. Large inflows concentrated over a short period can create future rollover risks when deposits mature simultaneously. Effective asset-liability management is therefore essential to prevent maturity mismatches.

Banks should actively engage with the global Indian diaspora through digital platforms, overseas branches, and targeted financial awareness campaigns. Enhanced outreach can help maximize participation before the expiry of the RBI's special window.

Financial institutions should also ensure that the liquidity generated through swap arrangements is directed toward productive sectors of the economy. Careful deployment of funds can improve profitability while minimizing credit and liquidity risks.

Additionally, continuous monitoring of global interest-rate movements and exchange-rate trends will be necessary to sustain the attractiveness of FCNR(B) deposits in a competitive international financial environment.

Conclusion

Foreign Currency Non-Resident Bank [FCNR(B)] deposits represent a strategic financial instrument that benefits both overseas Indians and the Indian economy. For depositors, they provide attractive returns, tax efficiency, full repatriability, and protection against exchange-rate fluctuations. For India, they serve as an important source of foreign currency inflows, strengthen foreign exchange reserves, improve banking sector liquidity, and support Rupee stability.

The RBI's decision to absorb hedging costs and provide regulatory incentives demonstrates a calibrated policy response aimed at enhancing external resilience while supporting domestic financial stability. If effectively implemented and supported by strong participation from the global Indian diaspora, the FCNR(B) initiative can play a meaningful role in strengthening India's macroeconomic foundations and sustaining long-term economic growth.